In March 10, 2023 Silicon Valley Bank (SVB) failed after a bank run. Two days later, Signature Bank was shut down. Then on May, 2023 regulators seized control of First Republic Bank and sold it to JPMorgan Chase. It was a good strategic decision to curtail the crisis. It could have rattled the US Financial system.

As the storm calmed down, let’s summarize and review the environment where and when these three banks has collapsed. More importantly, what are the lessons learned and identify the tools to prevent similar situation and , if unavoidable, at least minimize the impact.

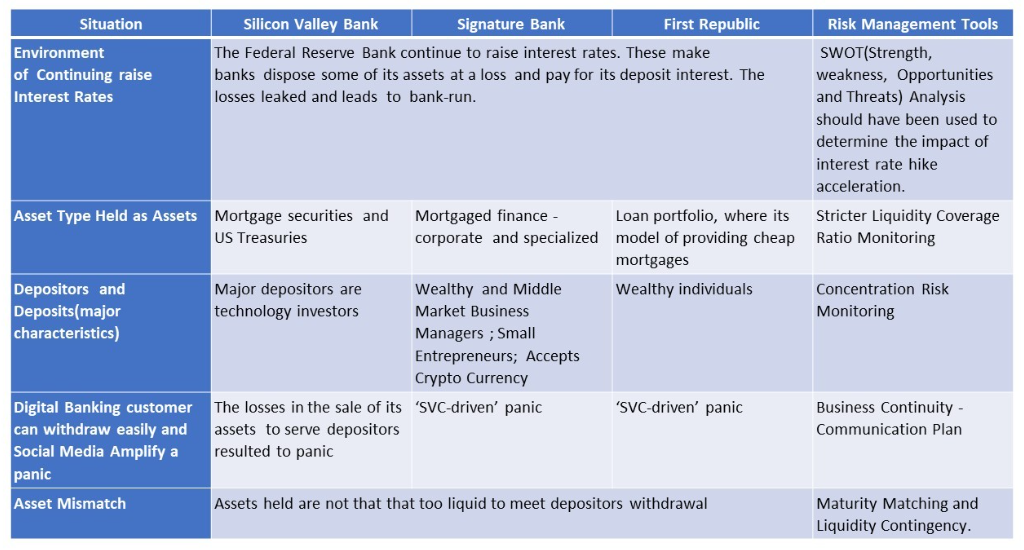

This table attempts to simplify and summarizes the crisis:

Regulators should consider the end to end impact before continuing the increase in interest rates. While it is understandable that inflation should be immediately addressed, it must be tiered and gradual, not in a sharp or steep mode. The first tool, SWOT Analysis could have captured what just happened.

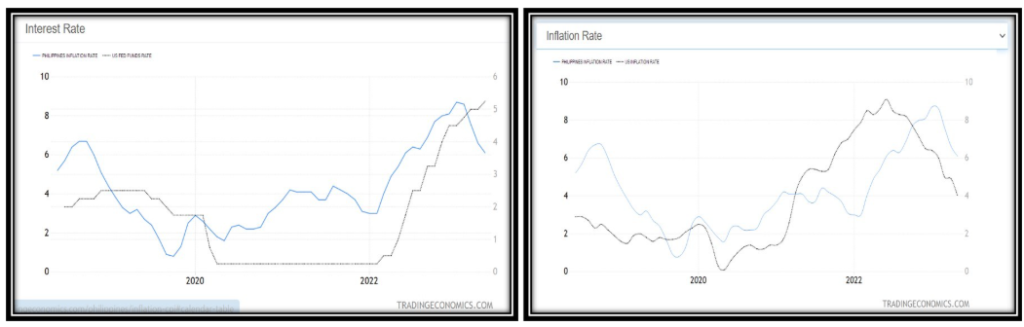

The graph below shows the historical US and PHL inflation rate and interest rate trends. The sharp increase in inflation is meet by increase in interest rate. While necessary, it could be also countered by gradual and planned interest rate increase with SWOT analysis before execution.

The second tool is Liquidity Coverage Ratio Monitoring. It should have been used in monitoring if there’s sufficient assets to meet withdrawals anytime. Regulators should have mandated banks to have more high quality liquid assets. In this way, banks can adapt to the steep increase in interest rates and eventually massive withdrawals.

The third tool is Concentration Risk Monitoring. As bulk of deposits are from certain industry and sectors, any adverse situation could impact the whole bank. Efforts should have done to balance not only the assets, but also deposits.

The fourth tool is Comprehensive Business Continuity Plan – Communication Strategies. Good communication strategies can allay the fears of depositing public and other stakeholders. The crisis emanate from knowledge of major depositors on the losses of the banks in the disposal of assets brought by steep increase in interest . The Business Continuity Plan(BCP) – Communication plan should have anticipated the leak and could have announced remedial plan. They could have elaborated that the situation is part of the stressed test and are manageable.

The fifth and last tool is Asset-Liability and maturity matching. The SVC case has a mismatched assets and deposits maturities. While related to Liquidity Coverage Ratio solution, more accurate asset and liability management tool on matching could have surfaced the imbalance. Solution could have been formulated at early stage.

The crisis has been over. The period of raising inflation and interest rate is still around. Nevertheless, it has been observed that the regulators are slowing down in raising of interest rates. In this regard, banks can manage well their assets and liabilities.

Again, the tools are SWOT Analysis, Key Risk Indicators on Liquidity Coverage Ratio and Concentration Risk, BCP-Communication Strategies and Asset & Liabilities Maturities Matching. Diligently use these tools moving forward.

Note: This article also appears in LinkedIn account of the author.

![]()

Clap

Clap